It’s important to understand what a good credit score is and what credit scores mean for your mortgage application and for your financial future.

A good credit score is important because it will have a major impact on your mortgage application and the interest rate that you will be given, which can result in thousands of dollars saved in the long-run. Let’s learn everything we need to know about Credit Scores in Canada.

- What is a credit score?

- Why is a credit score important in Canada?

- How can I check my credit score for free in Canada?

- How to build your credit history to get your dream home

- What credit score do you need to get a mortgage in Calgary, Alberta?

- Do late payments affect my credit?

- What is a hard credit check vs a soft credit check?

- What if you have an existing debt (for example, student debt or car loan)?

- How to improve my credit score?

1. WHAT IS A CREDIT SCORE?

In Canada, lenders determine your financial health and your ability to repay your debts/pay your bills on time by looking at your credit score.

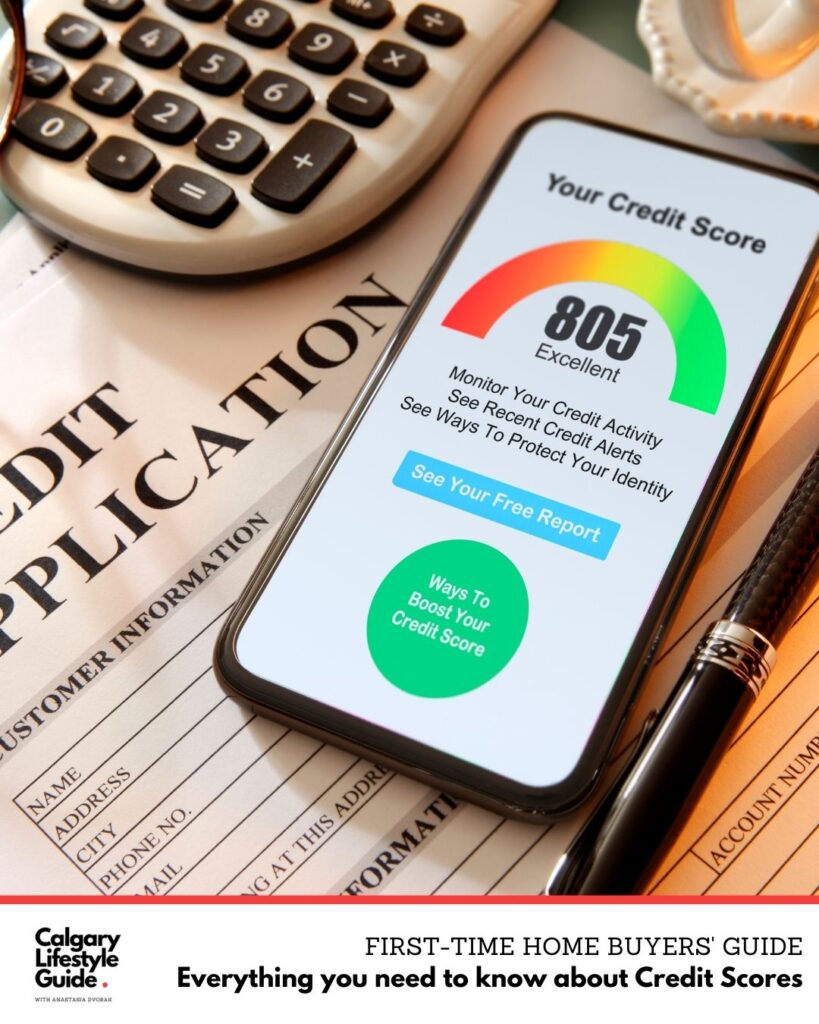

Credit scores range anywhere from 300 to 900 and the following categories are assigned to your credit score based on your financial health: poor, fair, good, very good.

Credit scores range anywhere from 300 to 900 and the following categories are assigned to your credit score based on your financial health: poor, fair, good, very good.

The higher your credit score, the better it is for you as lenders prefer to approve different types of loans and credit products for people who have good or very good credit scores meaning their financial health is in good shape (bills paid on time, not too much debt, etc).

A score of 650 and above is considered good and means that you are a low default risk customer and a good candidate for various types of mortgage or credit products (for example, leasing/financing a car, a cell phone, an appliance, etc.). The ideal credit score is 750 or higher.

- See also: Everything You Must Know Before Buying a Home for Sale in Crestmont Calgary

- 8 Tips on How to Choose a Calgary Community when Moving to Calgary

- Evergreen SW Calgary Community Tour (Evergreen Homes & Amenities)

- Top 5 Best Calgary Organic Food Stores/Organic Grocery Stores You Need to Check Out

In addition to looking at your credit score, the lenders will also take a look at your credit report that has all the information about any late payments, number of credit accounts you’ve opened (for example, it will show how many credits cards you’ve ever had), your overall debt levels and the length of your credit history.

2. WHY IS CREDIT SCORE IMPORTANT IN CANADA?

Many newcomers and people not well-versed in Canadian financial matters think that they don’t need to have any debt at all, so they avoid getting any credit cards or any loans.

However, if you ever want to get a mortgage or finance a car or even get a utility service set up (like gas/heat or a cell phone), you will need to have an active credit history that shows that you are capable of handling debt and paying it off on time.

Without an established credit history, you won’t be able to lease or finance a vehicle or get a new phone – you will have to pay cash upfront. You won’t be able to get a good mortgage rate because you have zero trustworthiness in the eyes of a lender.

3. HOW CAN I CHECK MY CREDIT SCORE FOR FREE IN CANADA?

Checking your own credit report DOES NOT affect your credit scores. It’s important to check your credit report at least every 6 months in order to identify any potential identity theft or mistakes in your file.

DOES NOT affect your credit scores. It’s important to check your credit report at least every 6 months in order to identify any potential identity theft or mistakes in your file.

In Canada, there are two major credit bureaus that you need to monitor and be aware of – Equifax and TransUnion. You can check your credit score and view your credit report immediately for free with several online companies such as CreditKarma.ca and Borrowell.com.

You can check your credit score and view your credit report immediately for free with several online companies such as CreditKarma.ca and Borrowell.com.

You can also request a free copy of your credit report every 12 months from Equifax and TransUnion.

When you are applying for a mortgage, your mortgage professional will be able to do a credit check and pull your credit score for you with your consent.

If someone asks you for a credit check, it means they want to see a copy of your credit report.

4. HOW TO BUILD YOUR CREDIT HISTORY TO GET YOUR DREAM HOME?

Start early and start building your credit history – it’s the best thing you can do for your family in terms of saving money in the long-term. I am not saying here you need to go crazy and get 10 credit cards – that’s actually the worst thing you can do!

Get one or two credit cards at maximum with a small balance on them and start paying them off. Make sure to use no more than 30% of your available credit card limit and make your payments on time.

Eventually, your credit card limit will increase meaning the bank trusts you enough and is willing to increase the maximum credit card amount that you can carry. You can also shop for various credit cards and choose the ones with the lowest interest rate.

5. WHAT CREDIT SCORE DO YOU NEED TO GET A MORTGAGE IN CALGARY, ALBERTA?

The minimum credit score needed to get a mortgage approval is between 620-680 but that depends on the lender.

The minimum credit score needed to get a mortgage approval is between 620-680 but that depends on the lender.

The higher your credit score, the more likely your lender will be able to provide you with the lowest mortgage rates in Calgary.

As a general rule, the lower your credit score is, the more costly it will be for you, so it’s better to work on improving your credit score and paying attention to your financial history.

6. DO LATE PAYMENTS AFFECT MY CREDIT?

Do you pay your bills on time? If not, your credit score will reflect that. If you know you won’t be able to pay your bills on time, it’s best to communicate with your bank or whoever this bill is owed to, so that you can make a delayed payment arrangement with them.

If you don’t do it, they can send your unpaid bill to the collections agency (a collection agency is a company that lenders use to recover funds that are past due or from accounts that are in default) and that can affect your credit rating.

If you don’t pay your outstanding bill, they can send your unpaid bill to the collections agency (a collection agency is a company that lenders use to recover funds that are past due or from accounts that are in default) and that can affect your credit rating.

According to Equifax, “late payments remain on a credit report for up to seven years from the original delinquency date – the date of the missed payment.”

7. WHAT IS A HARD CREDIT CHECK VS A SOFT CREDIT CHECK?

Every time a lender or creditor looks at your credit report, their inquiry is labelled in your credit report as either a hard inquiry or a soft inquiry. These inquiries have different effects on your credit history. Let’s see what that means.

HARD INQUIRY AFFECTS YOUR CREDIT RATING

When you apply for credit (mortgage, auto loan, credit card or some other type of credit), a lender reviews your credit report with your permission as a part of their decision-making process.

This type of inquiry is connected to an actual credit application and is usually labelled as “hard inquiry” and it appears on your credit report and can have a temporary, negative impact on your credit scores.

Hard inquiries stay on your credit report for over 2 years, but their impact is not as strong as time goes by.

One of the biggest mistakes first-time homebuyers do is that they buy expensive furniture, appliances or vehicles on credit during their mortgage application process. This is a big no-no as too many hard inquires in a short period of time can lower your credit score as this type of activity is concerning to lenders because they may think that you will have problems paying your bills as you are overspending.

One of the biggest mistakes first-time homebuyers do is that they buy expensive furniture, appliances or vehicles on credit during their mortgage application process.

This is a big no-no as too many hard inquires in a short period of time can lower your credit score as this type of activity is concerning to lenders because they may think that you will have problems paying your bills as you are overspending.

If you see a hard inquiry from a lender on your credit report that you don’t recognize, it is possible that someone is pretending to be you and is trying to get credit in your name which is a sign of identity theft. That’s why it’s important to be aware of what’s happening in your credit report.

SOFT INQUIRY DOES NOT AFFECT YOUR CREDIT RATING

A soft inquiry happens when you check your own credit or when a lender, an insurance company, or a credit card company gets access to your credit to approve you for various offers. Soft inquiries have no impact on your credit score.

Soft inquiries have no impact on your credit score.

Soft inquiries are not linked to a specific credit application for a new credit meaning that soft inquiries have no effect on your credit score.

8. WHAT IF YOU HAVE EXISTING DEBT (FOR EXAMPLE, A STUDENT LOAN OR A CAR LOAN).

It’s definitely worth it to improve your credit score and minimize your existing debt if you have any.

Existing debts make it more difficult to be approved for a good mortgage rate because the lender will need to consider your debt-to-income ratio and the mortgage stress test (mortgage stress test requires banks to check that a borrower can still make their payment at a rate that’s higher than they actually pay.)

9. HOW TO IMPROVE MY CREDIT SCORE?

If you have a lower or less than ideal credit score, it’s important to spend some time (at least 6 months) improving it. A good score can save you a lot of money in the end, so it is worth the effort.

Here are the following activities that will help you improve your credit score:

- Only apply for a credit if you need it

- Pay your bills in full and on time

- Do not carry a large amount of unpaid debt

- Review your credit report every 6 months or less and check for mistakes or identity theft

- Consider a secured credit card if you’re building from the ground up

- Use no more than 30% of your available credit card limit

- Don’t apply for too much new credit in a short amount of time

- If you’ll be applying for a mortgage or auto loan, be sure to do your shopping in a short time frame

- Shop for the right credit card with the lowest interest rate. Almost every bank has one but they don’t advertise it. Ask for it.

- Shop around for the lowest interest rate and a mortgage that has the best conditions for your situation

If you have the energy for only one thing, then make sure that your bill payments are all paid in full and on time. Your payment history is one of the most important aspects of your credit score.

If your payment is going to be late or if you have problems making payments, make sure to arrange a payment agreement with your bank, your credit card company or the lender that you owe the payment to.

If you don’t do anything, it will be much worse. The lender is usually understanding and is willing to work with you.

We’ve covered everything you needed to know about credit scores in Canada. I hope that this information will be useful to you when you are getting ready to purchase your first home.

If you have any additional questions about credit scores, mortgages, or purchasing your first home, please get in touch with me. I will connect you with my best mortgage broker that has helped many of my clients and saved many deals and thousands of dollars for my clients.

NEED REAL ESTATE ADVICE?

I am a licensed real estate agent/Realtor with CIR REALTY in Calgary, Alberta. I’ve been in real estate since 2011. Learn about me here.

If you want to get more information quickly and save yourself some time and effort, just send me a message, book an appointment with me (office or Zoom) or leave me a voicemail/send me a text message – 403.835.6913 (I do not always pick up my phone as I am busy with clients, so for the fastest response, it’s better to text me or schedule an appointment online), and I’d be happy to help you figure out the best type of property in Calgary for you and your family.

If you are curious about what’s on the Calgary real estate market right now and want to know about interesting and fun Calgary events, sign up for my “Calgary Weekly Events in Your Inbox” here: http://bit.ly/yyceventslist

What about you? Do you have any questions about credit scores?

Reply in the comments or tweet me @YYCLivingGuide or Instagram @CalgaryLifestyleGuide